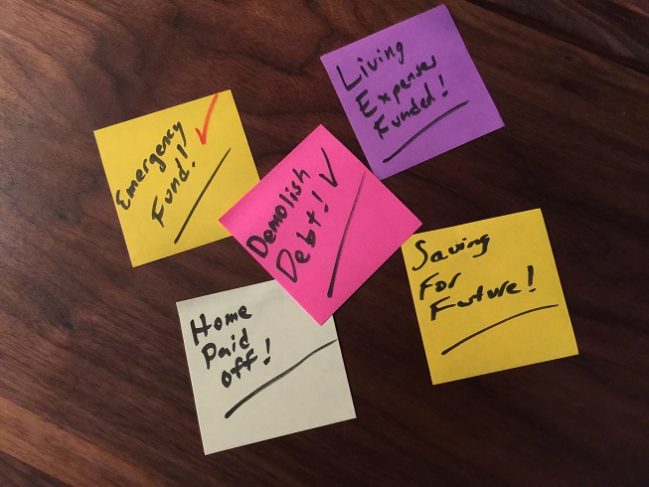

Creating money goals?

#1. Save an emergency fund.

#2. Pay off all of your debt (not including your home).

#3. Save 3 months or more of living expenses.

#4. Pay off your home.

#5. Begin saving 15% of your income.

#1. The Emergency fund: Every extra penny you have should be saved for this until it is fully funded. Dave Ramsey suggests a emergency fund of only $1000. I feel this is small for today’s possible issues. I suggest to save from $2000 to $3000. This will make you feel a lot safer and worry less. This will also help you to stay on #2. REMEMBER, this is called an emergency fund because it is for emergencies. Don’t dig into this to buy Christmas or birthday gifts. Taking a weekend vacation because you think you have earned it is not an emergency.

#2. Debt: This is an ugly word that we have been tricked into thinking it is a normal way of living. It makes me kind of sick just thinking about it. I suggest you do whatever you have to to stop watching commercials, reading magazine adds or even the adds in between videos on YouTube. They have spent a lot of time and money figuring out how to make you think you need all the latest gadgets and newest stuff.

If you want to retire early you will need to get rid of your old debt and stop creating new debt. But Dude, isn’t my house good debt? NO! Your home may be a lower interest rate, but it is not good debt. Quit spending your future income. Spending your future income, aka taking on debt, is pulling you down and placing a large burden on your future self. Just because you can get a loan does not mean that you should get a loan. Dude, I get it! No new debt, but how do I get rid of the old debt? If I make minimum payments it’ll take me 20 years to pay it off. Well friend, you can use the SNOWBALL method. I learned about this while reading “The Total Money Makeover”, by Dave Ramsey. List all of your debts with interest rates. Highest interest rate to lowest. Making the minimum payment on all but the highest and then throw all of your extra money at the highest interest rate. You can also pay off your debts in order of lowest to highest. Throwing all of the extra money at the lowest first. This is a good choice because it will give you a sense of satisfaction when you pay off some of the smaller debts quickly. Either way will work as long as you commit to one of them and stick to it.

#3. 3 months living expenses: This is in case of job loss. It is a larger safety net. It does not have to only be 3 months worth but it needs to be at least 3 months worth. If your monthly budget is $4000 then you will need $12,000. Don’t invest it, you need to be able to get to it if necessary. If you tie it up in a 6 month CD or in the stock market, you could have issues getting it when you need it. Put it in a savings account, you don’t need to keep it under your mattress.

#4. Paying off your home: Not much to say here other than DON’T BUY TOO MUCH HOME! Nobody’s impressed. Really, the bigness wears off. Just about when you have been in it a year and have to make the payments. Only buy the bare minimum. Don’t buy for future needs, when they come you can adjust if you feel you need to. Now with that said, If you already have a mortgage you need to pay it off (this can be different depending on your savings, income and age)

#5. Saving 15% or more of your income: At this stage it all depends on how fast you want to be able to retire. See chart, chart info taken from a mrmoneymustache blog The Shockingly Simple Math Behind Early Retirement.

| Savings Rate | Years Until Retirement |

| 10% | 51 |

| 15% | 43 |

| 20% | 37 |

| 30% | 28 |

| 40% | 22 |

| 50% | 17 |

| 75% | 7 |

Lets say you make $100k a year. If you are able to save 75% of your income it means that you are only spending 25% of your income per year to live. In 7 years you would have saved $525k. If you add in 8% interest per year it would be $797,747.07. If you lived off of the interest of that money at 8% interest you’d have $53,872 a year to live off of. If you made 6% – $44,122. Still more than enough to cover your $25k a year living expenses. You could even buy a new car or boat with cash every 3 years.

Of course what I have listed above does not include taxes. You may not make anywhere near $100k a year and you would need to have a paid for home to be able to live off of $25k a year. But this is meant to show you what is possible and the math behind it. It also shows you how flawed the current advise is as to how much you should be saving. The more you save the faster you will get to where you want to be. So is the new pool worth it? Yes, if your paying cash.

Hopefully I have covered this subject well enough. If you have any questions leave a comment below. I’m sure we’ll break this down further in later posts.

Thanks!

The Retirement Dude